Tyres Europe has published its Q1 2026 Quarterly Replacement Tyre Market Review, prepared by Astutus Research. This is what the data shows, and what it means for the rest of the year.

Consumer Tyres Return to Growth — Just

After a weak 2025, Europe's consumer replacement tyre market (passenger car, SUV and light commercial vehicles) edged back into positive territory in Q1 2026, rising 1% year-on-year to 58.1 million units. It's a modest number, but the direction of travel matters.

The recovery isn't uniform, though. The detail beneath that headline tells a different story:

- All Season tyres jumped 5%, continuing a multi-year trend as drivers favour the convenience and safety of a single tyre for year-round use.

- Summer tyres slipped 1%, losing further ground to All Season alternatives.

- Winter tyres fell sharply, down 14%, reflecting unusually mild conditions across much of Europe in the quarter.

The All Season segment is clearly not a temporary trend. It's reshaping how European consumers think about tyres.

Import Flows Are Being Redrawn — Fast

The import data tells a stark story.

Having jumped 26% in Q1 2025, PCLT (passenger car and light truck) tyre imports into EU27+UK fell nearly 22% in January–February 2026. Chinese-origin tyres drove most of the decline, falling 45%, with China's share dropping from 74% to 52%. An ongoing EU anti-dumping investigation had prompted heavy pre-buying of Chinese tyres throughout 2025, with concerns that duties could be back-dated. That pre-buying window is now closed.

ASEAN-origin tyres moved quickly to fill the gap, with their import share tripling from 7% to 21%, led by Thailand (+147%) and Vietnam (+165%). Cambodia added 0.4 million units from near zero. For truck and bus tyres, Thailand and Vietnam now hold over 63% of the EU27+UK import market between them.

This is a structural reorientation, not a one-quarter blip. The full report has the detail.

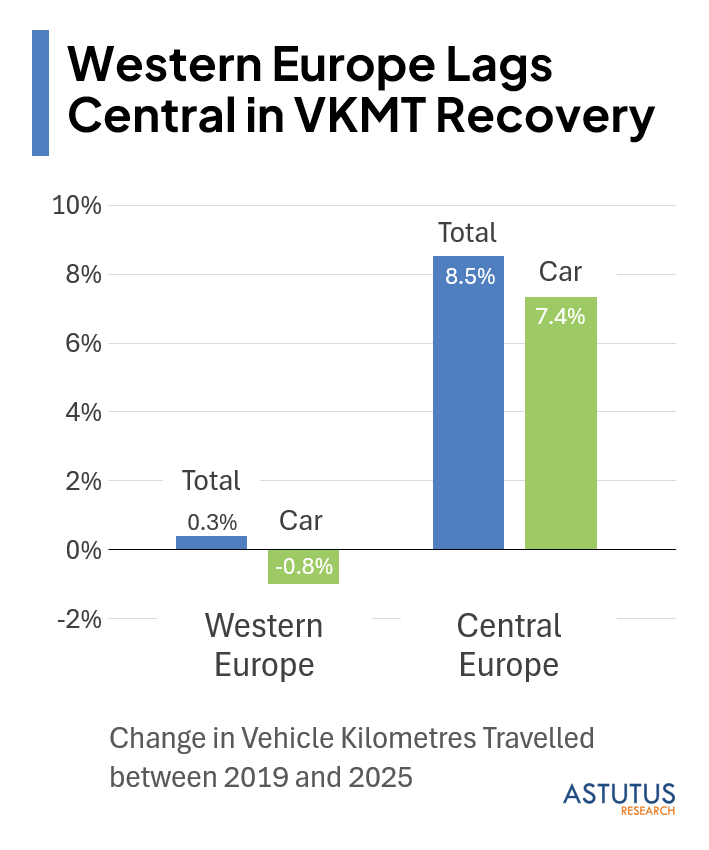

The Middle East Conflict Is a Lasting Headwind

Beyond Q1, the report flags a real risk: the Middle East conflict's impact on European miles driven.

Higher fuel prices began to bite from March, but the effect is expected to outlast the conflict itself. Futures markets point to a peak impact on oil prices this quarter, easing through to Q4, with a lingering tail into 2027. Embedded inflation and supply-chain disruption will continue to weigh on consumer spending and, by extension, on how much Europeans drive.

For the replacement tyre industry this matters directly: fewer miles driven means longer intervals between replacements, and in periods of economic pressure motorists tend to stretch those intervals further still.

The disruption hit early in the year, before the peak summer driving season, which limits the aggregate annual impact. But Q2 and beyond will bear watching.

Other Segments: Mixed Picture

Outside consumer tyres, the picture is varied:

- Truck & Bus tyres edged up 1%, supported by improving freight sentiment, though the Middle East uncertainty adds a cautionary note.

- Agricultural tyres declined 11%, with farm investment remaining subdued.

- Moto & Scooter tyres outperformed, rising 6%.

Sustainability: Stability at the Surface, Divergence Underneath

Europe generated around 4.4 million tonnes of used tyres in 2025, essentially flat year-on-year (+0.5%). But the headline masks significant regional divergence: Southern European markets (Spain, Portugal, Greece) and parts of Central Europe are growing materially faster, while larger Northern European markets including the UK, Germany and France saw little or no growth.

A decline in retreading has also increased the proportion classified as end-of-life tyres, adding pressure on recovery and recycling infrastructure.

This Quarterly Update has been prepared for Tyres Europe by Astutus Research, an independent provider of market intelligence focused on the tyre industry, mobility and tyre recovery & recycling. For further information contact info@astutusresearch.com or visit www.astutusresearch.com