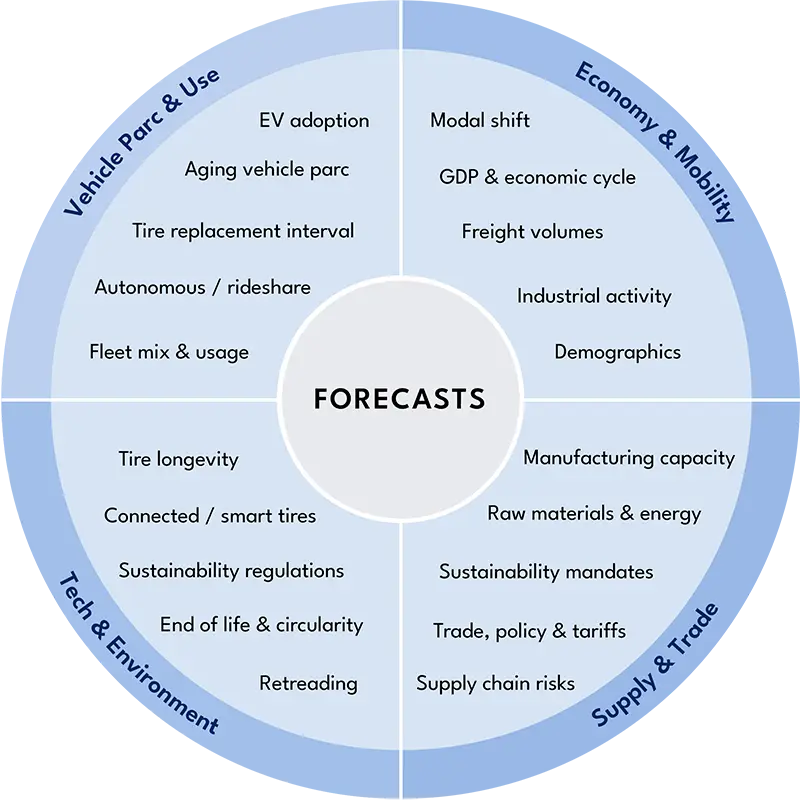

Low-cost imports, EV adoption, fleets, and regulation don’t move together — but they all affect forecasts.

Shifting trade flows shaped by import pressure, tariffs, and changing regulation are altering volume dynamics faster than planning cycles can adjust.

At the same time, EVs, fleets, and heavier vehicles are driving structural shifts in usage, replacement rates, and end-of-life flows.

The challenge isn’t modelling sophistication, it’s keeping inputs aligned with how the market is actually evolving.

Astutus Research exists to close that gap.

The Astutus Research data platform gives insights and strategy teams earlier, clearer signals on where tire and mobility demand is really heading before those shifts show up in sell-in, sell-through or parc data.

Powered by our proprietary Miles Driven (VKMT) data, discover underlying usage patterns across passenger cars, LCVs and trucks, cutting through noise from registrations, parc, and short-term sales effects.

By connecting Miles Driven with trade flows, replacement dynamics, and end-of-life outcomes, My Astutus explains why demand is changing, not just that it has.

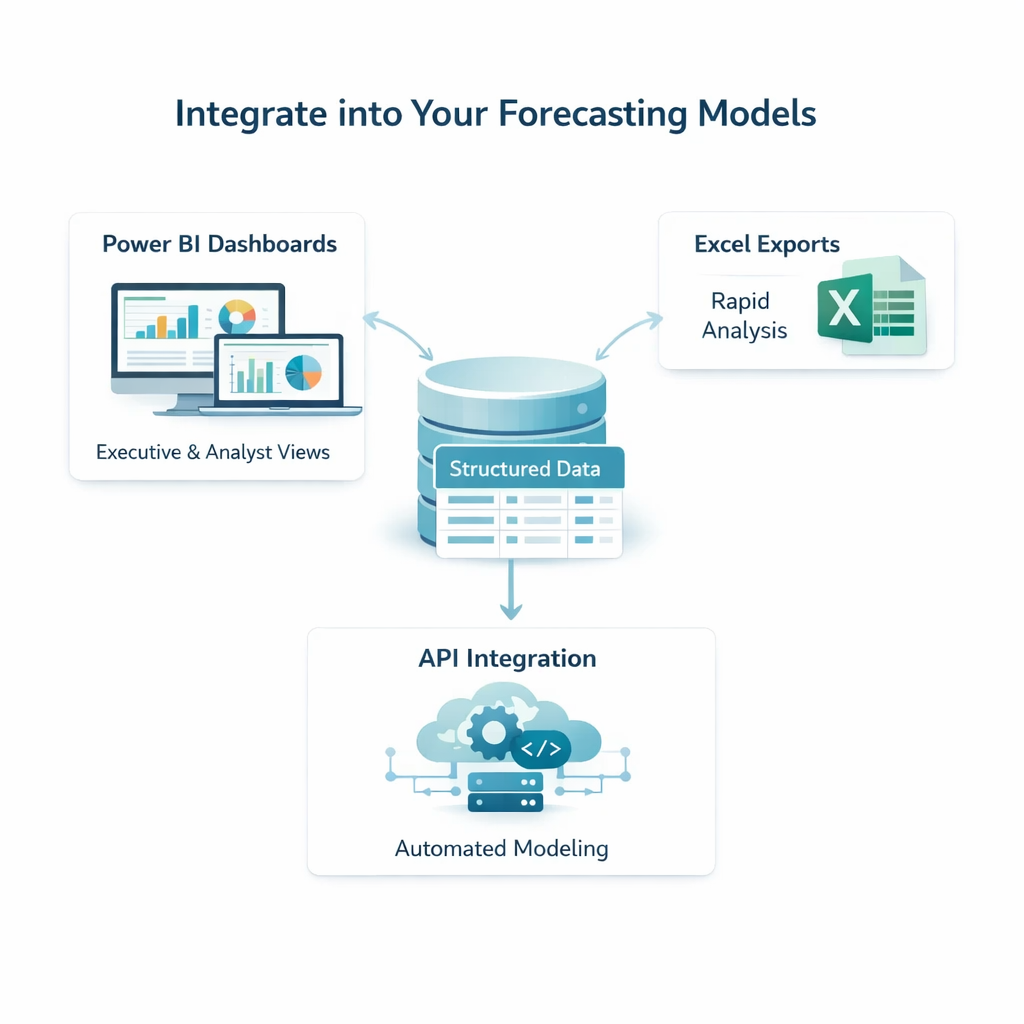

Structured, model-ready data fits directly into existing forecasting workflows, helping teams reduce uncertainty without reworking trusted internal models.

This is the impact of seeing demand shifts clearly before they show up in sales, parc or results.

Capacity investments were rephased after VKMT modelling revealed declining driving intensity avoiding overcapacity risk.

Sales efforts were refocused on fewer, higher-return markets after demand growth was ranked by VKMT, replacement dynamics, and regulatory risk.

Growth assumptions were stress-tested using independent VKMT and mobility data, leading to revised valuations and clearer downside risk ahead of investment committee approval.

End-of-life tire volumes were forecast by country, enabling better-timed investment decisions and avoiding early overcapacity as regulation evolved.

Independent market data strengthened credibility with regulators and delivered clearer, consistent messaging across member communications.

European replacement tyre demand returned to modest growth in Q1 2026, with consumer tyres rising 1% after a weak 2025. All Season tyres led the recovery, up 5%, while import flows shifted dramatically as Chinese volumes fell 45%. The Middle East conflict emerges as a key forward risk.

Q4 2025 confirmed three clear signals for Europe’s tyre market: persistent weakness, shifting seasonality, and continued pressure in freight and agriculture.

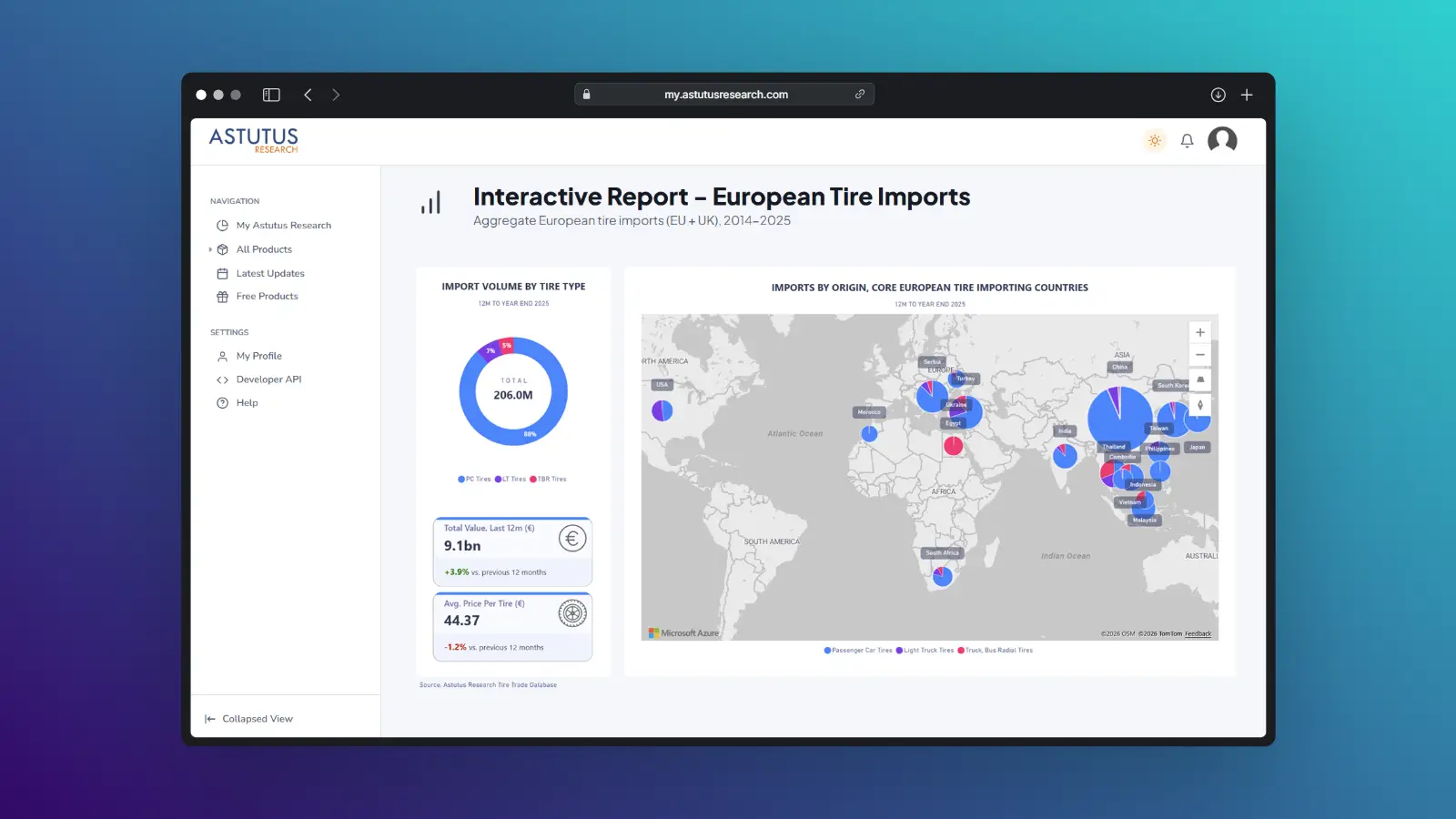

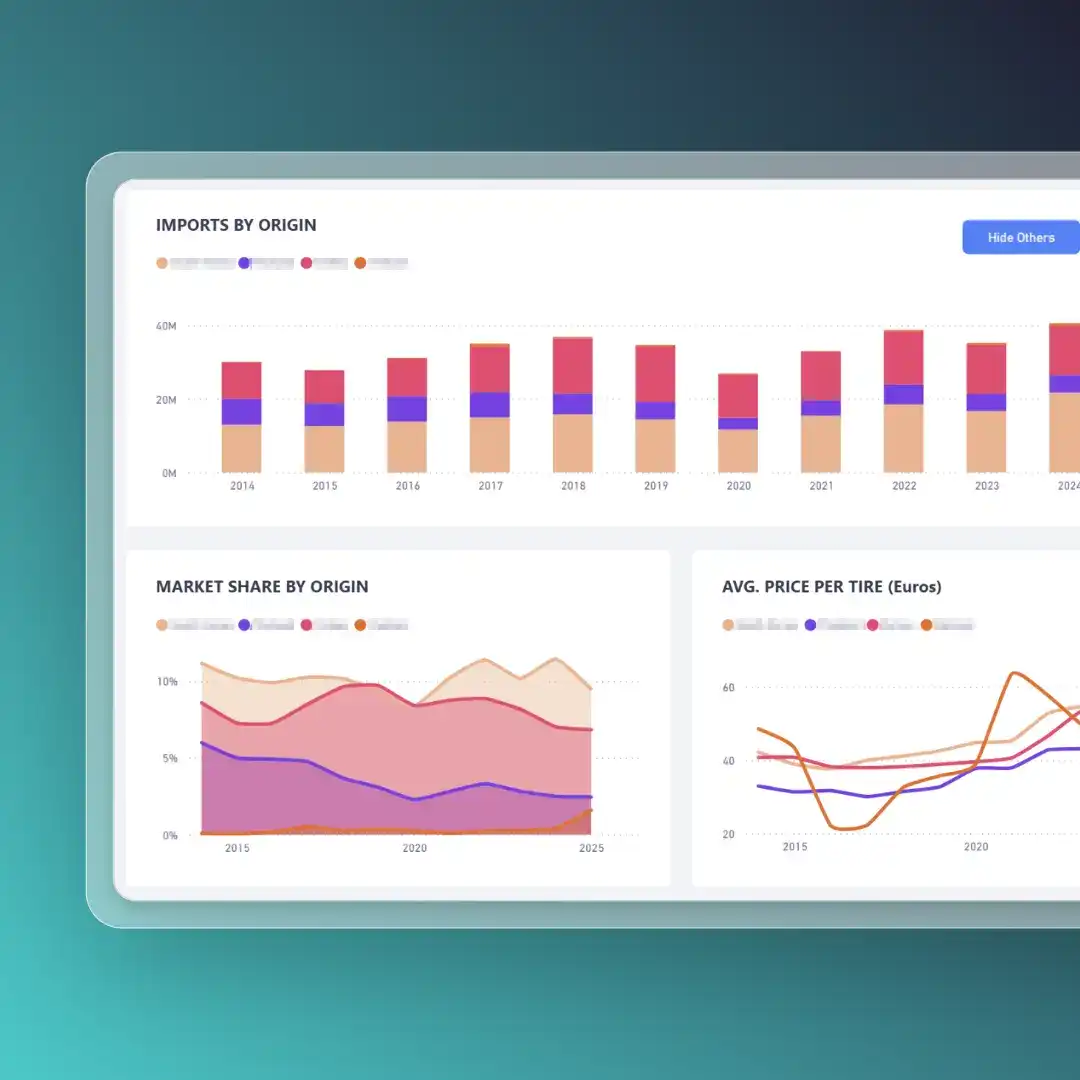

Record tyre imports into Europe in September were driven almost entirely by China, Serbia and Vietnam, while most other origins declined year-on-year. The surge appears tied to importers front-loading shipments ahead of the EU’s anti-dumping decision.